What RMB 3.1 Billion in Revenue and a RMB 182 Million Loss Reveal About the Bambu Effect

Creality 3D shipped 4.4 million 3D printers between 2020 and 2024 - more than any other company on the planet. On May 11, 2026, it passed its listing hearing for the Hong Kong Stock Exchange Main Board, clearing the final regulatory hurdle before what would be the first consumer 3D printing IPO in Hong Kong history. The prospectus that got it there, however, reads less like a victory lap and more like a war budget.

Revenue reached RMB 3.127 billion (~$447M USD) in 2025, according to the HKEX filing (etnet, May 11, 2026). But net profit swung to a loss of RMB 182.4 million. The company that once dominated global consumer FDM printing is spending aggressively - and the line items tell the story of an industry whose competitive center of gravity has shifted from hardware specs to software ecosystems.

The RMB 270 Million Marketing Line Item That Explains the Competitive Shift

Creality's marketing costs rose to RMB 270 million in 2025 - a 9x increase from 2022 levels, per the IPO prospectus (36Kr analysis via KR-Asia, March 26, 2026). R&D spending hit RMB 222 million, or 7.1% of revenue, up from 6.4% in 2022.

These are not organic growth investments. They are defensive expenditures driven by a single competitive force: Bambu Lab. The Shenzhen-based upstart, founded by former DJI engineers, reset the consumer 3D printing benchmark in 2022 with the X1 Carbon - a machine that combined multi-material printing, lidar-assisted bed leveling, and a cloud-slicing ecosystem that made the "it just works" promise real for the first time in the category's history.

The result appears starkly in Creality's own prospectus data. Its average selling price rose from RMB 1,306 in 2022 to RMB 2,404 in 2025, even as unit sales fell from approximately 842,000 to 742,000 over the same period (IPO Prospectus / 36Kr). Creality is selling fewer machines at higher prices - the opposite of what a volume leader wants - while spending nine times more on marketing to defend shelf space against a competitor whose software moat has proven difficult to replicate.

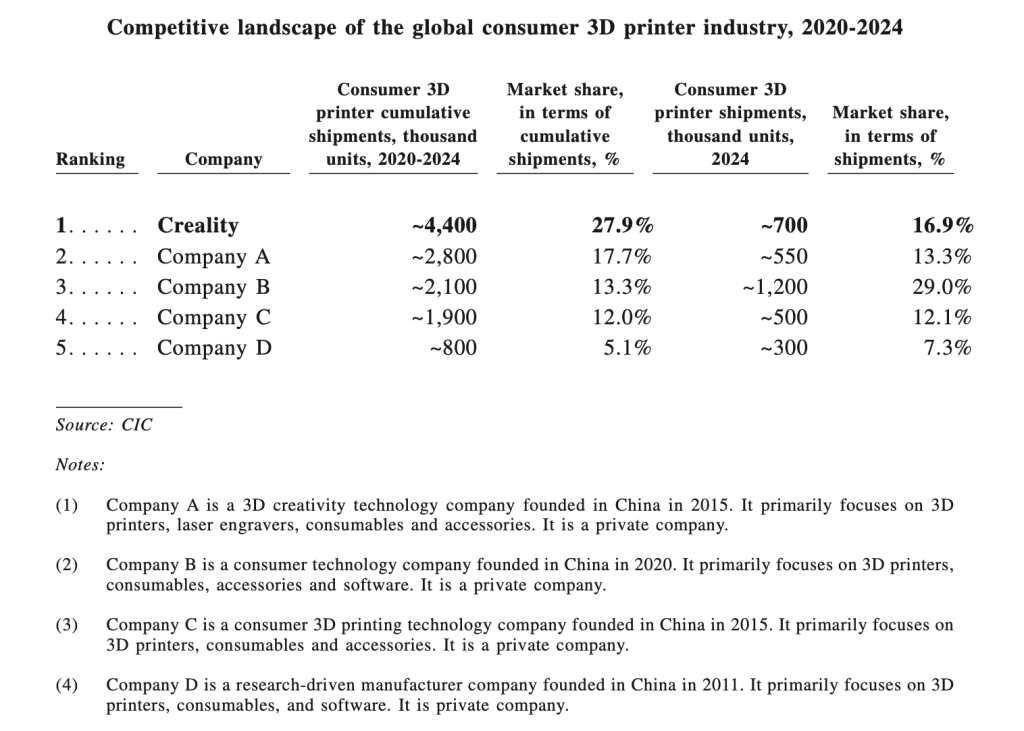

From 27.9% to 16.9%: How Market Share Erodes When Software Becomes the Product

Creality's cumulative market share of 27.9% across 2020–2024 still leads the industry, but the trend line is moving in the wrong direction. By 2024, its annual unit share had fallen to 16.9%, per the prospectus (CIC data cited in KR-Asia). Bambu Lab, which did not ship a single printer before 2022, captured approximately 29% of 2024 unit shipments - overtaking the former category leader in less than three years.

This is not a price war. Bambu Lab's machines sit at the premium end of the consumer segment. The competition is about workflow integration: cloud slicing, mobile app control, model libraries, failure detection, and the network effects of a growing user community. Creality's prospectus acknowledges this directly, noting that the company has invested in its Nexbie e-commerce platform and partnered with Tencent on AI-assisted design tools (KR-Asia, March 26, 2026). These are attempts to build the software layer that Bambu Lab had from day one.

The structural question for investors is whether a hardware company can retrofit a software moat, or whether the category has permanently bifurcated between the ecosystem leader and everyone else.

The Elegoo Signal and the Shenzhen Capital Cascade

Creality's hearing came days after Elegoo closed a 500 million yuan ($73M) B+ round led by Meituan, with the co-founder publicly admitting that the revenue gap with Bambu Lab had widened to 4:1 (3D Printing Industry, May 2026). The timing is not coincidental. Every consumer 3D printing company in Shenzhen except Bambu Lab is now raising capital to fund a software-driven catch-up.

The competitive dynamic is structurally similar to what happened in the drone industry a decade ago: DJI established a software-and-hardware integration moat that competitors spent years and billions trying to match, with most failing. Bambu Lab's founding team came from DJI. The playbook is familiar, and the early results - 29% market share in three years - suggest it is working again.

Creality's IPO will test whether public markets see this as a growth story or a margin-compression trap. The company's last private valuation was approximately $556 million (RMB 4B) in its 2021 Series A (IPO Prospectus). The IPO pricing will reveal whether that number holds, expands, or contracts under the weight of the Bambu effect.

What Eplus3D's Withdrawal and Elmet's Listing Tell Us About Investor Appetite

Two recent Chinese AM capital-markets events provide contrasting benchmarks. Eplus3D withdrew its $176.6M STAR Market IPO in early 2026, driven by regulatory scrutiny of receivables and export control dependencies (3D Printing Industry). Creality's consumer-facing business model avoids those structural headwinds - no defense exposure, no export license risks, no long-duration receivables from industrial customers.

But Elmet Group's successful $120.4M NASDAQ IPO in April 2026 sets a different kind of benchmark. Elmet succeeded because it had patented refractory metal technology, defense contracts, and profitability (3DPrint.com). Creality has scale and brand recognition but swung to a net loss. The contrast tests whether public markets reward category leadership and growth trajectory, or whether they now demand the IP moats and profitability that industrial AM companies demonstrated.

The global consumer 3D printing market is projected to grow from $4.1B in 2024 to $16.9B by 2029, a 33% CAGR per CICC (KR-Asia, March 26, 2026). If that forecast holds, category growth could lift all participants. But the distribution of that growth matters more than the aggregate number - and the early evidence suggests Bambu Lab is capturing a disproportionate share of the value.

The Counter-Signal: Installed Base, Direct Sales, and the Recurring Revenue Option

Creality is not starting from zero. Its cumulative 4.4 million units shipped represent real installed base and brand equity. The company's shift to direct online sales - from 14% of revenue in 2022 to 49% in 2025 - improves margin structure and customer data ownership over time (IPO Prospectus). The Nexbie platform and Tencent AI partnership could create a recurring revenue model that shifts valuation beyond hardware margins.

The risk is that these initiatives are catching up to a competitor that is already two generations ahead in software. Bambu Lab's cloud ecosystem, mobile app, and model library are not features - they are the product. Creality is spending RMB 270 million a year on marketing to defend against a company whose users market it for free through social media virality and community engagement.

No direct parallel in recent AM news captures this exact dynamic. The closest structural analogy is the drone industry post-DJI, but consumer 3D printing has different adoption curves, different switching costs, and a much larger addressable market if the category can expand beyond enthusiasts. Creality's IPO will be the first public-market test of whether that expansion is happening - and who is capturing its value.

IPO Pricing Will Determine Whether Public Markets Accept the Growth Narrative

The hearing pass clears Creality for listing, but the real signal comes in the IPO pricing and first trading days. The company's sponsor, China International Capital Corporation (CICC), will need to price the offering against the prospectus data that is now public: growing revenue, shrinking profits, and a competitive landscape where the category leader is spending heavily just to hold position.

If the IPO prices near or above the RMB 4B private valuation from 2021, it signals that public markets accept the growth narrative and the Bambu effect as a temporary competitive shock rather than a structural displacement. If the pricing comes in below that mark, or if the stock trades down post-listing, it suggests that investors see the margin-compression story as the dominant thesis.

Either outcome will set a valuation benchmark for the entire Shenzhen consumer 3D printing cluster - Bambu Lab, Elegoo, Anycubic, Snapmaker - and determine whether the next wave of Chinese consumer AM companies can access public capital markets. The hearing pass was the easy part. The pricing will be the signal.