Executive Summary: The Great Capital Divergence

January 13, 2026 – The prevailing narrative of the American and European additive manufacturing (AM) sectors in late 2025 has been one of consolidation - epitomized by ADDMAN Engineering’s recent acquisition of Forecast 3D to build a private-equity-backed super-supplier. However, a scan of market activity from January 9–12 reveals a fundamentally different strategy unfolding in Asia: Capitalization.

In a span of 72 hours, three major Chinese entities - Shining 3D, Eplus3D, and Xtool - have advanced significant Initial Public Offering (IPO) filings across the Beijing, STAR, and Hong Kong exchanges. This is not merely a financial maneuver; it is a structural divergence. While Western firms are contracting to protect margins, Eastern champions are tapping public markets to fuel massive infrastructure expansion. This "IPO Super-Cycle" suggests that the center of gravity for new capital formation in AM is shifting East, providing these firms with the war chests necessary to transition from hardware vendors to industrial infrastructure providers.

The Market Signal: The Public Market Trifecta

The signal is defined by the simultaneous maturation of three distinct verticals within the Chinese AM ecosystem: Metrology, Metal PBF, and Consumer/Prosumer hardware.

The Digital Anchor: Shining 3D confirmed it has surpassed 1.5 billion RMB (approx. $207 million USD) in annual revenue for 2025 as it moves toward the Beijing Stock Exchange. This figure is critical; it demonstrates that the "pick-and-shovel" strategy of 3D scanning and digital dentistry has achieved a scale of profitability that eludes many pure-play printer manufacturers.

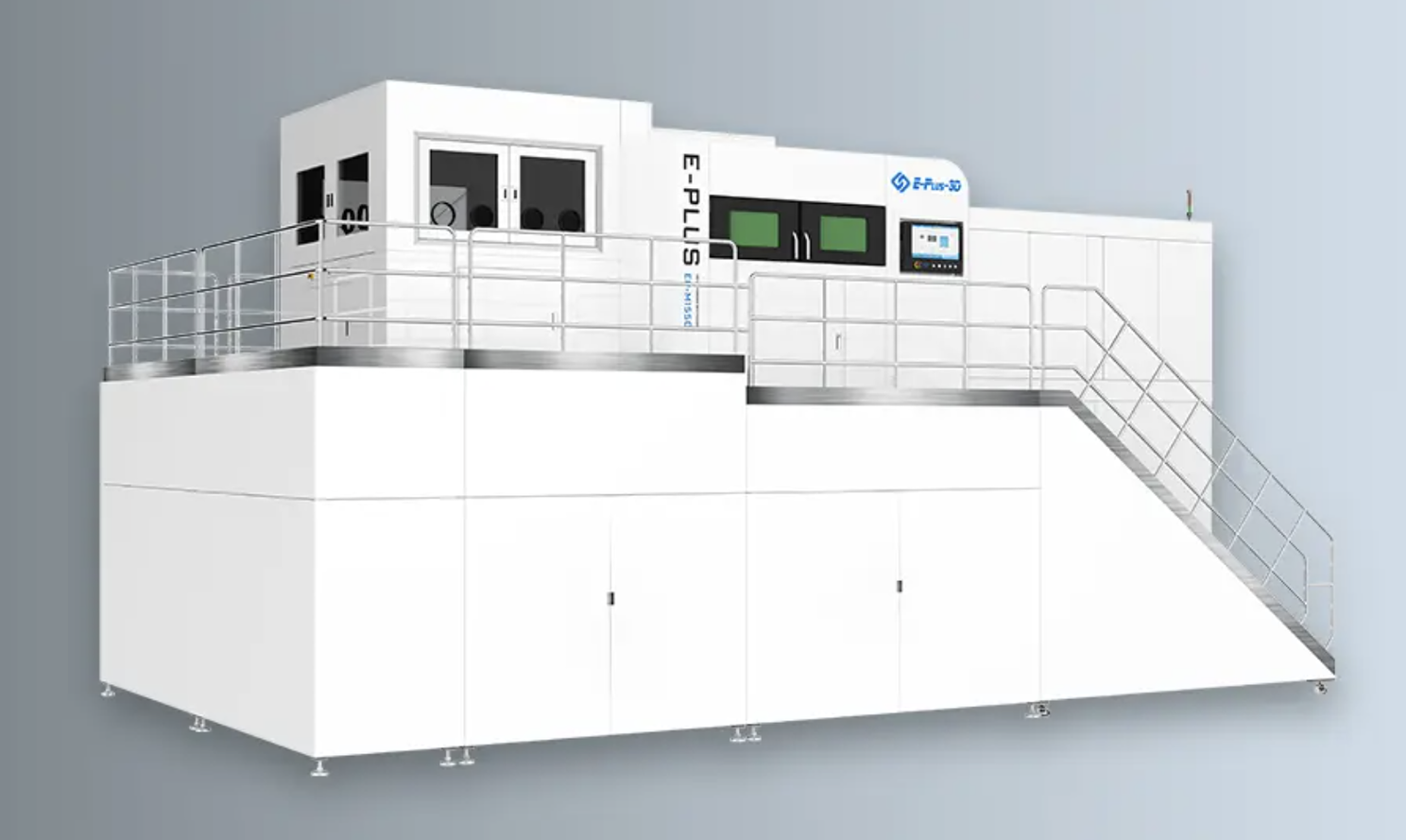

The Industrial Hammer: Eplus3D filed for its IPO on the STAR Market (Shanghai’s Nasdaq-style board), explicitly targeting the "100-billion RMB commercial aerospace sector." This listing is designed to fund the production of ultra-large-format systems, such as the 16-laser EP-M1550.

The Consumer Bridge: Xtool Innovate filed for a Hong Kong IPO following a massive $200 million USD Series D led by Tencent. This validates the "desktop factory" thesis, moving prosumer hardware from niche hobbyist circles to mass-market consumer electronics.

Strategic Analysis: Infrastructure over Innovation

The significance of these filings lies in the use of proceeds. Unlike the SPAC-driven bubble of 2020-2021, which funded speculative R&D, this capital wave is focused on industrial scaling.

1. The Aerospace Lock-in

Eplus3D’s move to the STAR Market is a direct play for aerospace dominance. By securing public capital, they can sustain the high inventory costs and long lead times required to manufacture gigafactories of metal printers. The mention of the EP-M1550 is vital; systems with 16+ lasers and build volumes exceeding 1.5 meters are no longer prototyping tools-they are infrastructure replacement for casting foundries. Eplus3D is effectively betting that public market liquidity will allow them to out-produce Western competitors who are constrained by tighter private equity covenants.

2. The 'Cloud Manufacturing' Reality

Supporting this hardware expansion is Winner Technology, which revealed it is scaling its capacity to 15,000 units, with 5,000 already operational. This is the "Foxconn model" applied to additive manufacturing. By integrating 15,000 physical nodes with SaaS scheduling, Winner Technology is creating a cloud manufacturing layer that competes directly with injection molding for low-to-mid volume production. The sheer volume of this deployment creates a barrier to entry that boutique service bureaus cannot breach.

3. The Material Vertical

This capitalization strategy extends to the raw material supply chain. Avimetal secured hundreds of millions of RMB in Series B+ funding specifically to verticalize the production of titanium and superalloy powders. In a market where powder cost remains the primary opex constraint (often 30-40% of part cost), controlling the atomization process allows these newly public OEMs to subsidize machine sales with lower operational costs-a classic "razor and blade" model executed at an industrial scale.

Contextual Synthesis: The Atlantic Divide

To understand the gravity of this shift, one must contrast it with the current state of the U.S. market.

On January 12, Black Buffalo 3D filed for Chapter 11 bankruptcy. Despite achieving technical milestones like ICC-ES AC509 certification for construction printing, the firm succumbed to the capital intensity of the sector. The lesson here is clear: in the U.S., high interest rates and risk-averse venture capital are starving hardware startups that cannot show immediate SaaS-like margins.

Conversely, the U.S. survival strategy is Consolidation. ADDMAN Engineering’s acquisition of Forecast 3D creates a formidable domestic supplier, but it is a defensive move - aggregating existing capacity to gain leverage with defense primes. It optimizes existing assets.

The Asian strategy is Expansionary. These IPOs are raising capital to build new assets. Eplus3D isn't buying a competitor; they are building a factory to produce 16-laser machines. Winner Technology isn't acquiring a service bureau; they are installing 10,000 new printers. This divergence suggests that by 2027, the installed base capacity - and therefore the volume production capability - may skew heavily toward the East.

Future Outlook: The R&D Capital War

The immediate impact of this "IPO Super-Cycle" will be price compression in the large-format metal segment. With Eplus3D and Avimetal capitalized, expect the cost-per-cubic-centimeter of printed titanium to drop, pressuring Western OEMs like EOS and SLM Solutions to respond.

Mid-term, the risk for the West is that "Capitalization" breeds "Standardization." If 15,000-unit farms like Winner Technology’s become the norm, they will set the data standards for distributed manufacturing. The company that owns the network - and the capital to maintain it - sets the rules. As 2026 progresses, the battle will not be fought over who has the best laser, but who has the deepest balance sheet to deploy them.

Analyst Note: Watch the stock performance of Shining 3D closely post-IPO. If it trades at a software-like multiple (due to its 3D scanning/data focus) rather than a hardware multiple, it will trigger a wave of imitators attempting to rebrand AM hardware companies as "Digital Manufacturing Platforms" to access similar liquidity.