From Fragile Supply Chains to 9-Hour Drone Bodies

The old way: a broken drone part means a 72-hour logistics chain across contested waters, with supply depots that make prime targets. The new way: a shipping container arrives at a forward operating base, prints a replacement fuselage in hours, and has a fully assembled aircraft ready the next day. That is the value proposition Firestorm Labs is selling with its $82 million Series B, announced April 29, 2026 - the largest dedicated funding round for expeditionary additive manufacturing to date.

The San Diego-based defense tech company, which began as a drone maker before pivoting to mobile production, has now raised $153 million total (TechCrunch, April 29, 2026). The round was led by Washington Harbour Partners with participation from NEA, In-Q-Tel, Lockheed Martin Ventures, Booz Allen Ventures, Ondas, Geodesic, and Motley Fool Ventures. The strategic investor mix - spanning intelligence community venture capital, prime defense contractors, and consulting firms - signals that expeditionary AM has moved beyond experimental curiosity into something the Pentagon is actively funding.

How xCell Compresses the Drone Supply Chain

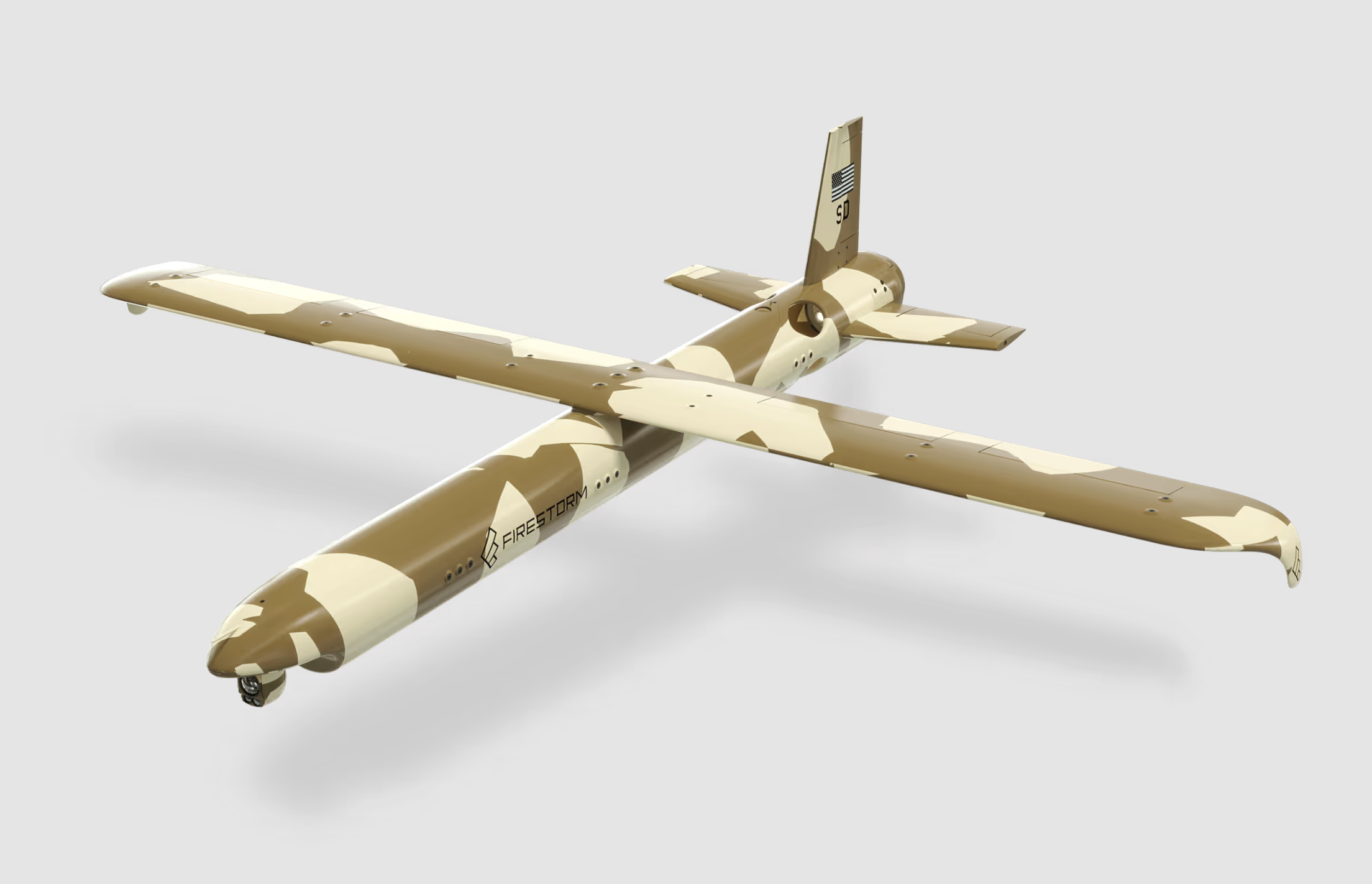

Firestorm's core platform is xCell, a containerized manufacturing system housed in a standard 20-foot shipping container. Inside sits an industrial HP Multi Jet Fusion 3D printer - secured through a 5-year global exclusive for mobile deployment applications - along with post-processing and assembly workspace. The company's flagship output is the Tempest drone: a 55-pound unmanned aircraft with a 6-foot fuselage capable of long-range missions and a substantial payload (Tech Funding News, April 30, 2026).

The production timeline is the headline number: drone body printed in under 24 hours, with full assembly completed shortly after (TechCrunch, April 29, 2026). That compression matters because it changes the operational calculus. Instead of stockpiling drones at centralized depots - which become high-value targets - a commander can print mission-specific configurations on demand. The Tempest is not locked into a single role; depending on mission requirements, it can be configured for surveillance or electronic warfare, CEO Dan Magy told TechCrunch.

The company has grown its workforce substantially in the last 12 months (Morningstar/ACCESS Newswire, April 29, 2026). Two xCell units are currently deployed domestically - at AFRL in Rome, New York, and with AFSOC in Florida - with operational deployment in the Indo-Pacific theater (TechCrunch, April 29, 2026).

Containerized AM Competitors: SPEE3D, Craitor, and the Marines

Firestorm did not invent the factory-in-a-container concept. SPEE3D's Expeditionary Manufacturing Unit (EMU) - a cold spray metal printer in two 20-foot containers - has been deployed with the U.S. Army, British Army, and during RIMPAC exercises since 2023. Craitor's FieldFab system brought containerized FDM/FFF for field repair to Army units starting in 2022. What differentiates Firestorm is the integration of industrial polymer MJF throughput with a purpose-built drone production workflow, plus the capital scale to move from demonstrations to theater-wide deployment.

The timing is not accidental. The same week Firestorm announced its Series B, the U.S. Marine Corps launched a two-week field exercise (April 28–May 8, 2026) at Camp Pendleton deploying a containerized AM ecosystem with EOS, Markforged, BigRep, and 3YOURMIND for expeditionary maintenance and drone production (TCT Magazine, April 30, 2026). The exercise, run by 1st Maintenance Battalion, I Marine Expeditionary Force, validates the same operational concept through a separate DoD branch - containerized AM at the tactical edge is a cross-service priority, not a single-company narrative.

The macro funding context reinforces the trend. The DoD FY2026 budget allocates billions to additive manufacturing projects, with a significant year-over-year increase, and "Contested Logistics" designated as a Critical Technology Area (3D Printing Industry, 2026). The Pentagon is actively seeking expeditionary AM solutions, and Firestorm's raise positions it to capture a share of that demand.

The Bull Case: First Mover in a Protected Market

The strongest argument for Firestorm is the convergence of capital, strategic partnerships, and procurement momentum. The HP exclusive is particularly significant: Multi Jet Fusion is the most production-proven polymer AM technology for end-use parts at scale, and locking it into mobile deployment for five years creates a barrier to entry. Any competitor wanting to match Firestorm's throughput in a containerized form factor would need either a different technology (cold spray, FDM, SLA) or a separate licensing deal with HP.

The strategic investor lineup also provides a path to revenue. Lockheed Martin Ventures gives Firestorm a channel into prime contractor supply chains. In-Q-Tel provides intelligence community credibility. Booz Allen Ventures brings consulting relationships across DoD branches. These are not passive checks - they are market-access mechanisms.

The Tempest drone itself addresses a genuine operational gap. The U.S. military's demand for attritable unmanned systems - cheap, expendable aircraft that can be risked in contested environments - is growing rapidly. Programs like the Air Force's Collaborative Combat Aircraft (CCA) and the Replicator initiative are driving demand for drones that can be produced quickly and deployed in volume. Firestorm's model of printing them at the point of use eliminates the logistics vulnerability of shipping finished aircraft across the Pacific.

The Bear Case: Unquantified Economics and Scaling Risk

The counter-signals are substantial. Firestorm has not disclosed xCell unit economics, throughput per container, or production volumes. The "factory in a container" narrative is compelling, but without data on cost per part, utilization rates, or maintenance requirements, it remains a story rather than a proven business model. The company has only two deployed units domestically and an unspecified number in the Indo-Pacific - not yet a fleet.

The 5-year HP exclusive is a double-edged sword. It provides technology differentiation, but it also creates single-supplier dependency. Any disruption to HP's MJF supply chain - powder availability, printhead replacement cycles, software updates - directly impacts xCell operations. In a contested logistics scenario, that dependency becomes a vulnerability.

The contract structure also warrants scrutiny. Firestorm holds a USAF contract with a substantial ceiling, but only a fraction has been obligated (TechCrunch, April 29, 2026). That gap between ceiling and obligation is common in early-stage defense procurement, but it means the company is still in the demonstration-to-production transition, not full-rate production. The path from 2 deployed units to theater-wide deployment is unproven, and startup scaling of defense hardware has a poor track record. Beehive Industries faces similar skepticism about production qualification for its 3D-printed Rampart engine, and the broader SPAC-era AM cohort - Desktop Metal, Velo3D, Markforged - demonstrated how quickly deck-driven narratives can collapse when production reality fails to match projections.

The Global Parallel: SPEE3D's Head Start, Firestorm's Capital Advantage

The closest comparator for Firestorm's trajectory is SPEE3D, the Australian cold spray AM company that has been deploying containerized metal printers with Western militaries since 2023. SPEE3D's EMU has logged real operational hours - British Army field trials, U.S. Army evaluations, RIMPAC exercises - and has a technology (cold spray for metal parts up to 40kg) that Firestorm's polymer MJF cannot match for certain applications. But SPEE3D has not raised anything close to $153 million, nor does it have an exclusive partnership with a printing technology giant.

The comparison illuminates the strategic trade-off. SPEE3D has more field experience and a metal-capable platform; Firestorm has more capital, a higher-throughput polymer process, and an integrated drone production workflow. The two are not direct substitutes - they address different parts of the expeditionary AM mission set - but their parallel existence confirms that the containerized manufacturing category is real and attracting serious investment. The question is whether Firestorm's capital advantage translates into faster deployment and better unit economics, or whether SPEE3D's head start in operational qualification proves more durable.

What the Series B Does and Does Not Prove

The $82M round is a strong signal - not yet market-defining. It accelerates an existing trend (expeditionary AM) with the largest dedicated capital deployment to date, backed by strategic investors who can open procurement channels. But it does not prove that the xCell platform works at scale, that the unit economics are viable, or that Firestorm can navigate the defense hardware scaling gauntlet that has claimed so many predecessors.

The next 18 months will be decisive. If Firestorm converts its USAF contract ceiling into obligated production contracts, deploys xCell units across multiple theaters, and discloses credible throughput and cost data, the thesis strengthens considerably. If the company remains at 2–5 deployed units with undisclosed economics by late 2027, the narrative will look increasingly like the SPAC-era promises that failed to materialize.

For now, the factory fits in a container. The question is whether it fits the Pentagon's production requirements.