XTPL Reports Q1 2026 Revenue of PLN 1.6M, Adds Semiconductor and Defense Customers for ODRA Platform

Hardware

Originally reported by 3DPrint.com

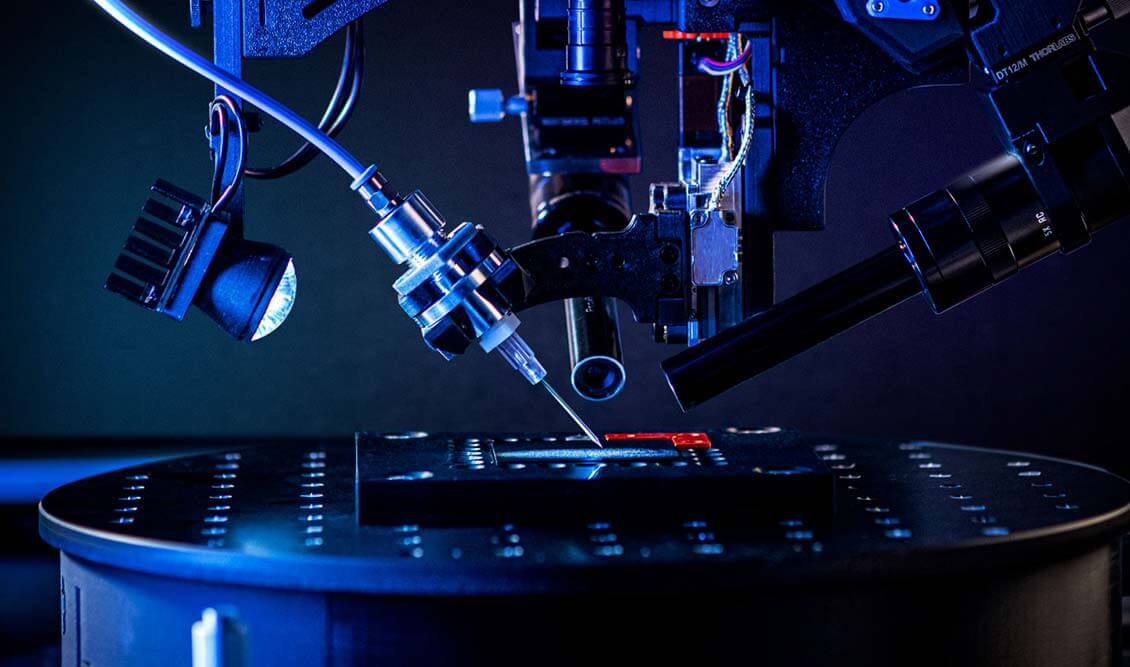

Polish microprinting specialist XTPL (WSE: XTP) reported Q1 2026 revenue of PLN 1.6 million ($441,000), with product and service sales contributing PLN 1.2 million. The company delivered its Delta Printing System (DPS) and Ultra-Precise Dispensing (UPD) modules, and secured the first order for its new ODRA low-volume production platform from a Silicon Valley customer in semiconductor advanced packaging with defense ties. CEO Filip Granek confirmed a UPD module is now operating on an active industrial production line at a major Chinese display manufacturer, marking a transition from lab to fab. XTPL also raised nearly PLN 30 million ($8.3 million) via a public share offering and Polish NCBR support to fund UPD deployments, ODRA development, and DPS sales expansion.

This quarter matters because XTPL is threading a narrow needle: its micrometer-scale conductive printing targets semiconductor and advanced electronics manufacturing-verticals where AM adoption is still rare outside niche applications. The ODRA platform, priced at more than double the DPS system, is designed for real production environments rather than R&D, which directly addresses the industry's long-standing gap between prototyping credibility and production repeatability. The defense-linked customer in Silicon Valley and the active Chinese display line both signal that XTPL is moving beyond the "promising technology" phase into commercial validation, though revenue remains modest. The company now has four commercial product lines, but its cash position of PLN 2.1 million and EBITDA loss of PLN 3.9 million mean the recent capital raise is essential to sustain parallel commercialization efforts.

From a practical standpoint, XTPL's near-term execution risk is high: it must convert the current customer evaluations into repeat orders, particularly for ODRA in defense and UPD in China, while managing cash burn until those revenues materialize. The "lab to fab" claim is credible for the UPD module now on a Chinese production line, but the company needs to demonstrate that this translates into recurring revenue rather than a single integration project. For buyers evaluating microprinting for semiconductor packaging or advanced displays, XTPL's technology is now referenceable in production, but the small revenue base and reliance on further capital mean procurement decisions should weigh technical fit against supplier stability.

This article is an AI-assisted rewrite of the linked source report. Facts originate from the source; phrasing is AMPulse's. Use Read Original below to verify, or Report an issue if something is wrong.

Topics